Pilot Launch | Pairing AI climate alerts with resilient liquidity for MSMEs in Kenya

AI-powered weather and flood alerts help microentrepreneurs prepare for climate shocks before they disrupt their businesses.

Mercy Corps Ventures supported Atram and Fortune Credit in launching a pilot, alongside partners PayPal and Humanity Insured, testing whether AI-driven weather alerts, preparedness advice, and emergency credit can strengthen MSME resilience to floods

This post is the first in a two-part series; the second will share key insights after the pilot is completed. Written by Njeri Muhia, Pilot Manager at Mercy Corps Ventures.

In brief:

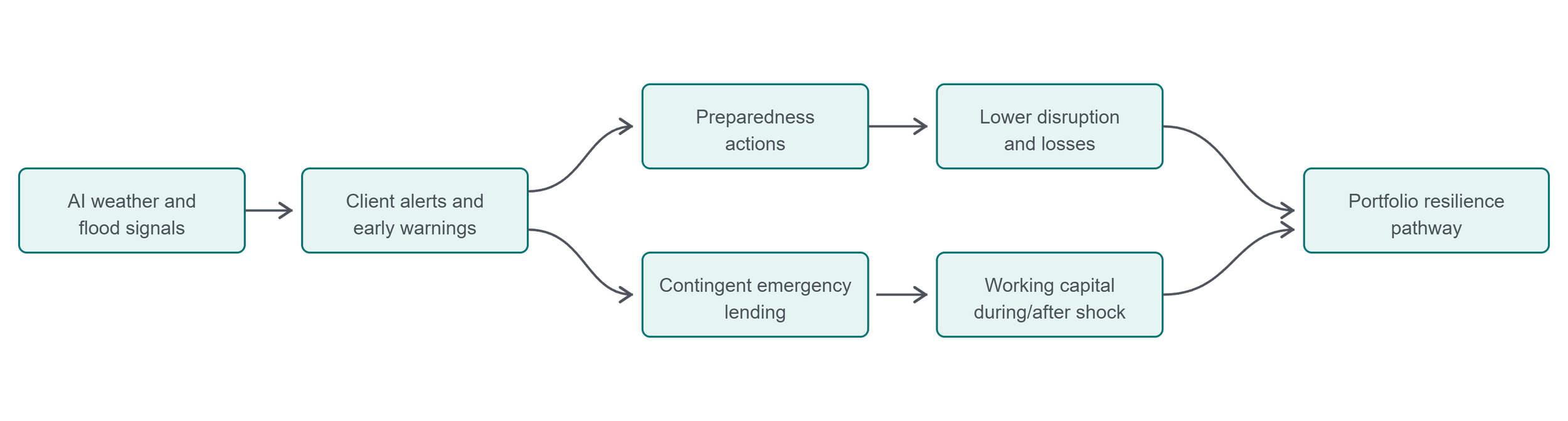

Atram and Fortune Credit are testing a combined climate resilience model with over 10,000 users pairing AI-driven weather alerts with preparedness advice, and action incentives, as well as Rain Cash preparedness loans

By tying portfolio risk protection mechanisms to heavy rain and flood forecasts and events, the pilot tests whether microfinance providers can support MSMEs before climate shocks become business and repayment crises

Climate shocks can disrupt businesses, damage inventory, and threaten livelihoods.

The Problem

In Sub-Saharan Africa, over 44 million MSMEs remain perilously under-protected against the rising tide of climate shocks. Africa is warming faster than the global average, and extreme weather events are becoming more frequent. In East Africa, floods have more than tripled in frequency over the past 30 years, from an average of less than 3 floods per year in the 1980s to roughly 10 floods per year now. Kenya is highly exposed: a single season of torrential rains in 2024 led to floods that affected 800,000+ people, causing over 300 deaths and displacing 100,000 individuals. Moreover, flooding in Kenya has historically led to substantial economic losses–in 2024, a staggering 79% of MSMEs suffered revenue losses exceeding 40% due to the flooding crisis.

Such climate events have human and economic stakes that are impossible to ignore. When a major flood hits, a shopkeeper can see her entire inventory destroyed overnight, or be forced to shut her doors for weeks. Women-led businesses often suffer the most, as they tend to have fewer assets and less access to finance, compounding their vulnerability. In short, climate change is turning weather disasters into financial disasters for millions of micro-businesses.

Surveys in Kenya and Uganda found that preparedness remains shallow: 65% of respondents had accessed climate information, but only 36% reported taking action to prepare, and 58% said they did not have a business continuity plan. At the same time, digital lenders have seen loan default rates soar from 15 to 20% in 2020 to nearly 40% by 2024; as climate-driven income shocks intensify borrowers’ vulnerability and make credit less affordable and accessible for those most at risk. Moreover, A 2021 study found that only around 17% of SMEs in Kenya accessed loans for climate adaptation and many were forced to downsize or sell assets to cope.

The Pilot

Through the Fast Liquidity and AI for Shocks, or FLASH, pilot, Atram and Fortune Credit are testing a two-part climate-resilience model for microfinance customers during Kenya’s March-May 2026 rainy season. The pilot will reach up to 10,000 existing Fortune Credit clients across 18 flood-prone branches in Kenya, primarily micro-entrepreneurs, market traders, boda boda riders, working capital borrowers, farmers, and women-led small businesses whose incomes and repayment capacity are exposed to heavy rain and flooding.

The first layer is anticipatory: AI-led weather and flood alerts designed to help micro and small businesses act before heavy rainfall turns into business disruption. At the center of this layer is the Fortune Weather App, powered by Atram. Clients receive invitations to get the app through SMS and their loan officers. Once onboarded, they can share their location, receive hyper-local weather and rain and flood alerts, review preparedness advice, and access weather-triggered support.

In practice, that could mean moving stock, protecting equipment, adjusting procurement, planning household cash flow, or documenting exposure early enough to reduce downstream losses. The second layer is financial response, if forecasts indicate heavy rains and flooding in Fortune Credit’s operating areas, this capital is immediately made available for emergency micro-loans to affected clients.

The pilot brings these two layers together through four connected components:

Protect: Up to 10,000 existing Fortune Credit clients receive access to AI-powered weather and flood alerts, forecasts, preparedness advice, and recovery guidance. Clients who do not use the webapp still receive SMS alerts.

Preparedness incentives: Clients may receive small, conditional cash incentives of KES 3500 when they complete and verify recommended preparedness actions, such as moving stock, protecting inventory, improving drainage, or taking other practical steps before heavy rain. These payments test whether small incentives can increase protective behavior at a cost lower than the losses avoided.

Rain Cash: Up to 500 eligible clients may access short-term emergency loans of KSh 5,000-15,000 before or after verified weather risk. Rain Cash is intended to help clients prepare for heavy rain, protect inventory, relocate assets, or restart trading after disruption. Clients apply through USSD, and disbursements are made through Fortune Credit’s standard M-Pesa channels. All credit decisions remain with Fortune Credit.

Portfolio shock protection: Atram and Fortune Credit are testing selective portfolio protection mechanisms, including loan moratorium and forgiveness, offering protection for clients who prepared but still experienced severe verified loss. These mechanisms are designed to help Fortune Credit to continue serving vulnerable customers while managing climate-driven portfolio volatility.

Perhaps the most innovative aspect is the pilot’s built-in loan forgiveness option. If a borrower is severely impacted by flooding – for example, if their business premises are destroyed or income is completely disrupted – Atram’s fund can step in to repay some or all of that client’s loan on their behalf. Together, these components bring several innovative approaches to climate-responsive lending:

Data-driven climate triggers: The pilot uses early warning systems and weather data (e.g. rainfall thresholds or flood forecasts)

Risk-sharing and loan forgiveness: Atram’s capital acts as a first-loss buffer – absorbing defaults or forgiving loans for borrowers hit hardest by floods. This risk-sharing gives Fortune Credit confidence to lend in high-risk contexts and it spares vulnerable clients from catastrophic debt.

Seamless client experience: Borrowers interact only with familiar, local financial services: the Fortune Weather App, SMS, USSD, M-Pesa, and Fortune Credit’s normal lending platform.

Key partners and their roles include:

Atram: A climate protection platform for lenders in emerging markets that helps financial institutions see which of their customers are exposed to climate shocks like floods, and give those customers early warnings, simple ways to prepare, and access to emergency liquidity. By building this into the institutions people already rely on, Atram turns climate risk from a driver of defaults into a way for financial services providers to protect their customer base.

Fortune Credit: Fortune Credit is a trailblazing micro-finance institution on a mission to catalyze economic empowerment among Kenya’s rural population. Their commitment to offering tailored credit and insurance services is driving positive change across Africa, not only economically but also ecologically.

Humanity Insured: Humanity Insured helps vulnerable communities access insurance - not just for recovery, but to build long-term resilience, helping people prepare, recover from disasters, but build long-term financial resilience to confidently prepare for and thrive despite environmental volatility

Our Hypotheses

AI-powered early warning systems and preparedness advice can increase preventive action among climate-vulnerable borrowers. This will be measured by:

% of clients taking at least one verified preparedness action

% of users reporting increased perceived preparedness

Alert-triggered app opens, forecast views, and advice interactions

Early access to Rain Cash and climate-linked liquidity can reduce business disruption and support faster recovery. This will be measured by:

Average reported asset loss during floods or heavy rain

% of alerted users reporting reduced or avoided climate-related losses

Rain Cash applications, approvals, repayment rates, and client-reported usefulness

Preparedness incentives can increase verified preparedness actions in a cost-effective way. This will be measured by:

Difference in preparedness action completion between incentivized and non-incentivized clients

Number and total value of incentives issued

ROI of preparedness incentives, measured as avoided loss value divided by incentive cost

Portfolio shock protection mechanisms can reduce repayment volatility and increase lender confidence in climate-linked financial products. This will be measured by:

Default rate or NPL volatility among protected clients or branches

Use of restructuring or grace periods after climate events

Fortune Credit’s operational readiness and willingness to scale climate-linked lending products after the pilot

Our Learning Questions

Do clients open, trust and act on alerts?

Does providing flood-triggered emergency loans (with Atram’s guarantee) help maintain repayment rates and business continuity for microentrepreneurs during extreme weather events? In other words, can this model prevent spikes in defaults and keep MSMEs afloat through a crisis?

How do borrowers perceive and value the loan moratorium and forgiveness feature? Do women and youth entrepreneurs, in particular, find it increases their sense of security?

The pilot will generate evidence on how anticipatory climate services can strengthen business resilience

Looking Ahead

This pilot will provide a first look at whether AI-powered alerts and preparedness advice, rapid liquidity, and risk-sharing mechanisms can help underserved businesses prepare earlier, recover faster, and remain connected to formal credit after climate shocks. By tying credit to climate triggers and sharing risk through external capital, we aim to test whether microfinance can become a more practical climate adaptation tool for MSMEs in vulnerable markets.